The damage is done, you're honestly reporting damage from the declared disaster for your primary residence. You followed all the instructions you were given by FEMA for your short term disaster recovery.

But what happens when you don't hear from FEMA in let's say 30 days, maybe 60, or even 90 days? How about 2 years later finding out you do not qualify for HUD CDBG-DR Grants because your FEMA Verified Loss (FVL) was $0.00 and reported by the FEMA inspector that was out to your property years ago.

A simple mistake, anyone could make it. But you weren't aware that your period to file an appeal has past and your disaster for FEMA is closed.

Here's some numbers to show you that this is not unusual and you need to stay on top of things when it comes to your declared damage or FVL. Keep in mind you are going to be looking at Major to Severe damage which is 12 inches of water and/or $8,000 in disaster related damages.

Here's a copy of our numbers in Louisiana for the 2016 floods.

- FEMA IA Registrants 193,000

This is the total number of households that registered with FEMA.

- FEMA Verified Loss 112,000

This is what FEMA determined out of the IA registrants how many homes had damage. This is your first appeal step if you were excluded by not having any damage related to the disaster if you know differently.

- Homeowners with Major or Severe Damage 57,631 (covers all homes, 12" or more of water and / or $8,000 or more in damages.)

- Homeowners with Major or Severe Damage without NFIP 36,510 (No Flood Insurance, 12" or more of water and / or $8,000 or more in damages.)

Using our numbers above we had 81,000 homeowners denied by FEMA's Verified Loss process and damage determination. It's hard to believe we would have 81,000 homeowners going through all the trouble to report damage that FEMA declared minor or less. Out of the 112,000 homes that FEMA inspected and found damage we had 54,396 homes that did not meet the required 12" or more of water and/or $8,000 or more in damages. That could have been 54,396 appeals and 54,396 contractor estimates for repairs. I can assure you that we did not have enough licensed contractors to write 54,396 work estimates so many people just stopped and gave up on the recovery programs. From the start, in Louisiana we have had 92% of all effected homes disqualified for one reason or other.

Don't take this lightly, it's going to be a long hard fight for you and your family.

You have a limited time to appeal, you have limited appeals. Ask people that have fought and won their appeals before you attempt to go it alone. It's a group effort and for about 92% of our 2016 homeowners they found out it takes a group to make change too late to make a difference.

When FEMA does a damage assessment and it's not Major / Severe or it's been more than 2 weeks since you have heard anything start calling and emailing. If you don't, it's going to all come out of your pockets soon enough.

Homeowners View and Understand of FEMA Verified Loss

We understand, between looking for a replacement vehicle because yours was flooded and keeping your job by being at your job during the day you may not fit the perfect FEMA person on site 24/7 as I was here in Louisiana.

- FEMA has to verify your losses (FVL) and it's not only for eligibility for FEMA temporary disaster assistance. You will have to schedule a time to be at home with the FEMA inspector.

The inspector is going to look for disaster related damages so don't do the old, "My siding washed away" when it is clearly something that happened years ago.

- FVL will play a major part of your long term disaster recovery with HUD CDGB-DR grants. If you don't get an IA or IHP grant you may not have been inspected or you may not have had the damage amount required to be accepted into the program.

FEMA is only your temporary fixers and that's really overstating things at times.

- They are going to look to see if your home is Safe and can be sanitary with normal or extra cleaning.

- They will check doors, windows, roof. If your doors open, even if they are slightly damaged that's not damage, if your windows are not broken and open as designed they are not damaged, if your roof has an old blue tarp on it, don't think they don't know the difference between a old roof leak and a new one.

- They check to make sure your interiors exterior walls are Ok, your ceiling is Ok. It can be old and sagging to the ground and be Ok in some cases.

- Do you have your electricity, gas, and they make mention to heat, plumbing and sewer.

Be very careful on AC, Heaters, Water Heaters, Filters, if it wasn't damaged by the disaster it's not covered by the IHP grant and may count against you when other long term assistance becomes available to you. You don't have to shower with cold water if your hot water heater just happen to break. But don't buy a larger more costly replacement if you have to pay out of pocket for it later and don't have the funds available. Get just what you need for your current needs. We have 2 people and a 6 gallon hot water heater. Keep out of pocket costs down.

FEMA's Safe, Sanitary and functional line, to me meant that the river wasn't in the house, the roof and walls were not ready to collapse and doors and windows would open, that's it.

Now, FEMA may tell you they will replace your heater and hot water heater if it was damaged by the disaster. Just as long as you know if your insurance later says they will replace it the FEMA IHP grant money then becomes a duplication of benefits. But not to worry, if you used FEMA grants on the hot water heater and your NFIP gave you money for a hot water heater simply take the NFIP amount and repair something that is not covered by your NFIP money that FEMA would allow you to repair. That is how you correct DOB issues from day one.

FEMA may say you can replace flooring, we found concrete works best the first year then sub-floors under the floors you pulled up and discarded because they were damaged. Floors that are visibly damage by the disaster can be repaired with FEMA grants but they would be wasted if in 6 months you found additional issues and had to pull up your flooring. Be careful not to replace over wet wood.

FEMA and your Windows: FEMA says if they are broken from the disaster. If the window was soaking in flood waters for days it's going to be replaced with HUD - CDBG-DR grant money but if they work, open and close, are not anything you can not repair with a piece of wood I would hold off on buying windows until you know about other parts of your home. Use the FEMA for structural repairs that need it because of the disaster and if your windows need replacing then do it. But be sure you understand that if they are damaged by flood waters and still sort of work, HUD grants will pay to have them replaced because of the water level in your home then when it's time you'll be awarded about $185 per window and that FEMA money you didn't have to spend is still in the bank to pay for upgrades or items HUD is not going to cover.

You will have to be at the property to meet with your inspector.

- The inspector is not a FEMA employee but a independent contractor trained to do what an insurance adjuster may do.

- They will have a tablet, ask you for permission to enter your property and have you sign some papers.

- They will not discuss anything with you because really, they are only data collection people.

- The inspector will have photo ID in view at all times.

- If you are not sure it's really a FEMA inspector call the Disaster Fraud Hotline: 866-720-5721.

- You will be asked to show proof that you own your house. If the house is not in your name show your name or an id with the address then have the FEMA contractor call the number on that is listed on your account to reach the homeowner to be authorized to allow the inspector on the property.

FEMA will do all the phone verification you need if you the owner can not be at the property. But you will need someone that can prove they are over 18 years of age and can allow FEMA on your property.

- Your inspector may take pictures, FEMA claims up to 5 pictures, I didn't count but the inspector will take pictures of your property. It's all for documentation.

- If you miss your inspection reschedule as soon as possible. You have to get this completed.

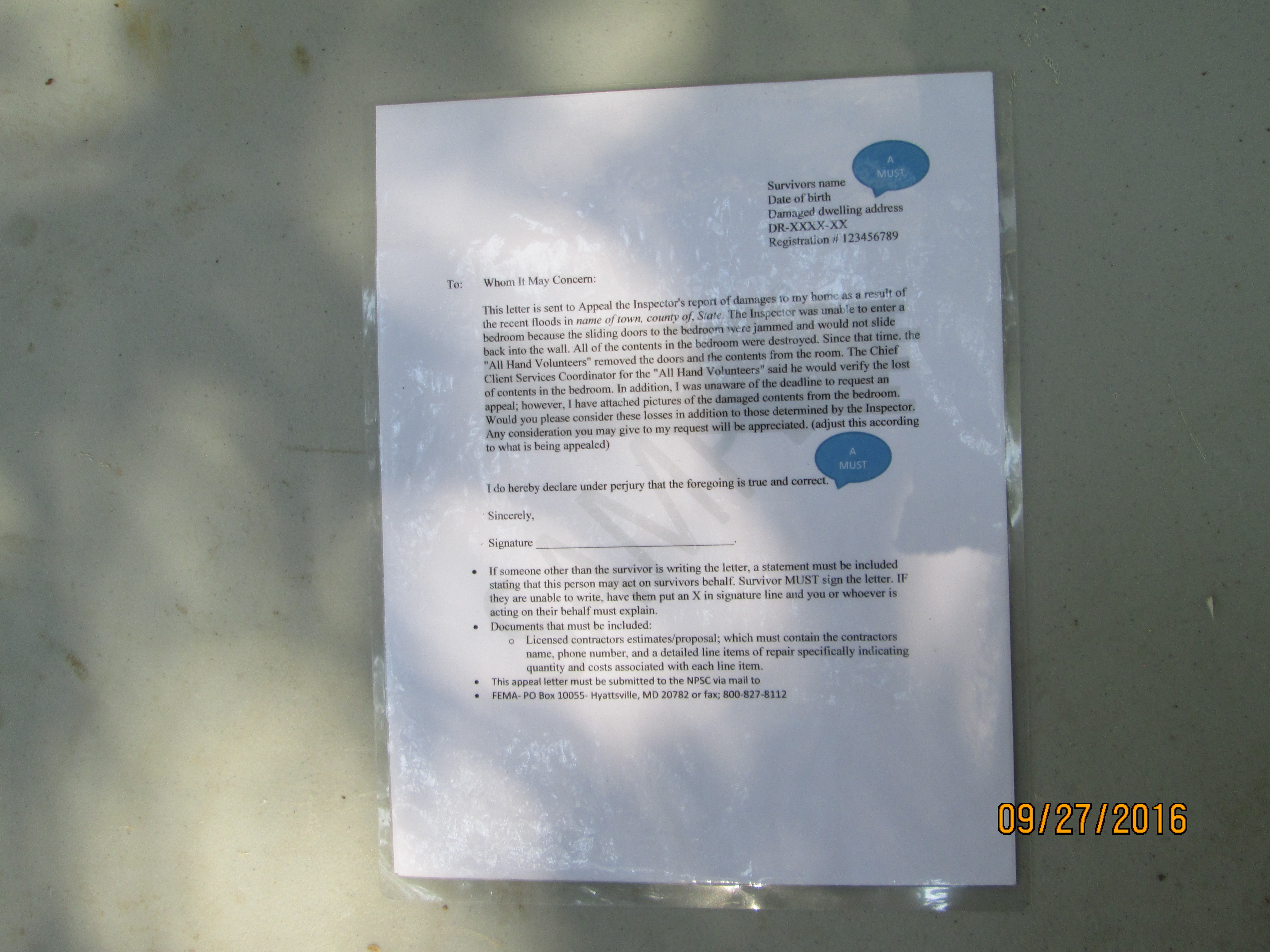

If you do not agree with the FEMA determination letter you have to call FEMA and talk to them. You may be able to clear things up by talking.

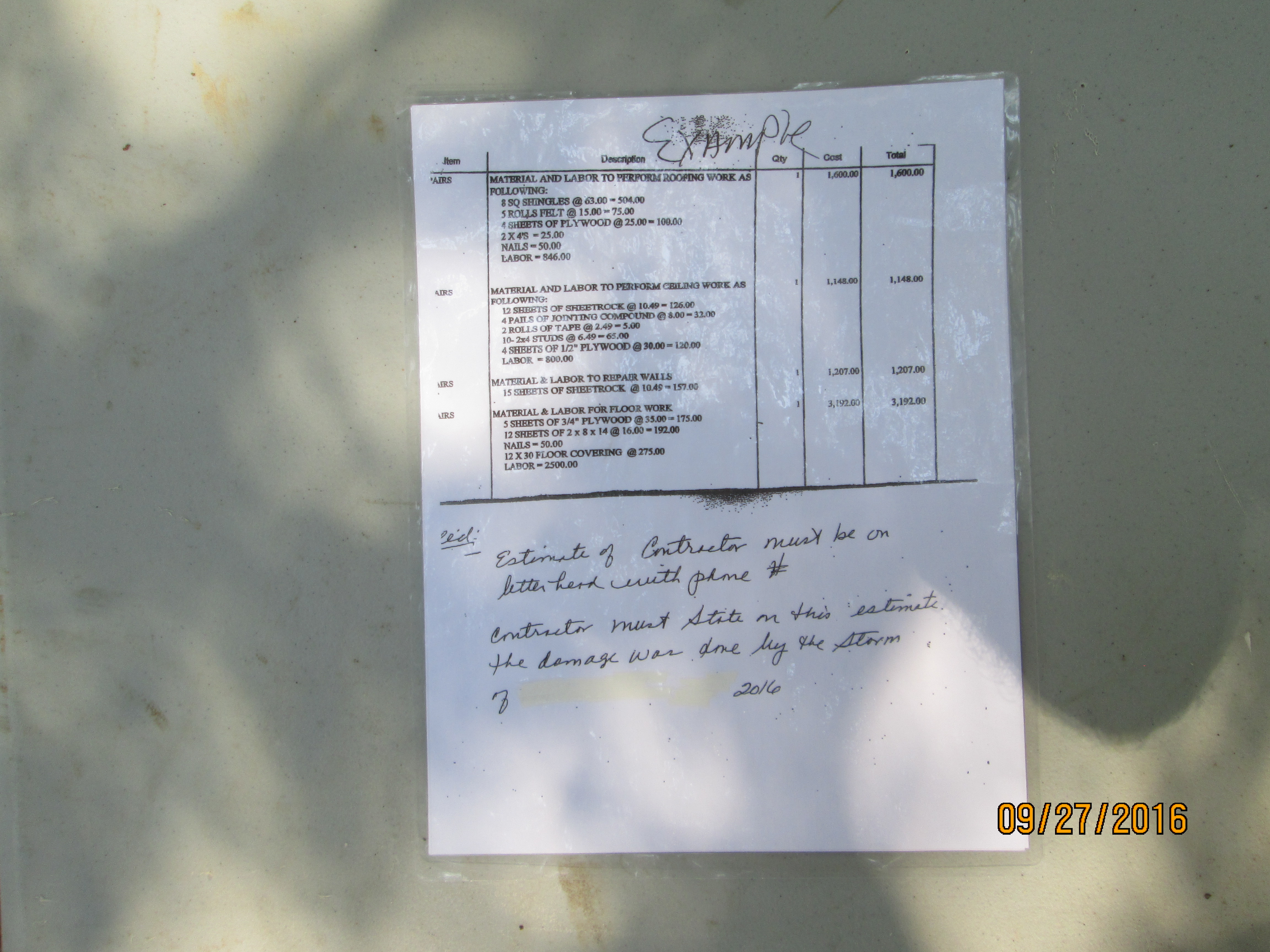

But, if your FEMA status can not be changed over the phone, you have to appeal in writing to FEMA and it has to be within 60 days of receiving your determination letter.

FEMA may take up to 90 days to respond. Use the same documents as a reference of what is required.

FEMA National Processing Service Center

P. O. Box 10055

Hyattsville, MD 20782-7055

Appeals may also be faxed to: 800-827-8112, Attention: FEMA. You can also call the helpline at 800-621-FEMA (3362) or TTY 800-462-7585 or visit a Disaster Recovery Center, where you can talk with someone about your particular case.

=========================

More information and a resource: (Case 1:06-cv-01 521 -RJL Document 3-3 Filed 08/31/2006)

"3. Within about 10 days of the inspector's visit, you will receive a letter from IHP informing

you of the decision on your request for help.

- If you are eligible for help, the letter will be followed by a U.S. Treasury/

State check or there will be a transfer of cash to your bank account. The letter

will explain "what the money can be used to pay for You should use the money

given to you as explained in the letter

- If you are not eligible for help, the letter will give the reason for the decision. You will be informed of your appeal rights in the letter from FEMA.

- If you were referred to the Small Business Administration (SB A) for help from the SBA Disaster Assistance Program, you will receive a SBA application. "

This is not a new problem: This is from a lawsuit filed in Louisiana back in 2006 after Hurricane Katrina. One year later when HUD CDBG-DR grants become available. If your FVL is not correct you are out of a possible $150,000 in grant money from the HUD CDBG-DR Grant program. FEMA did not notify every homeowner of the right to appeal their FVL determinations. This was in 2006, today for our floods of 2016 we have people denied assistance that would have qualified if they were aware of their rights to appeal the FEMA FVL determination.

"Plaintiffs' complaint alleges that the Federal Emergency Management Agency ("FEMA") violated plaintiffs' due process rights by failing to provide specific, comprehensive explanations for why it determined that plaintiffs were ineligible for housing assistance under Section 408 of the Stafford Act, 42 U.S.C. § 5174 et seq., and failing to provide adequate notice of plaintiffs' right to appeal such determinations. "

Resources:

{kind=link}

{kind=link}