"...if they could afford to repay the loan..."

"It's reasonable to think that SBA sort of did underwriting..."

This is what HUD training contractor CFI International presented by Bonnie Lester a consultant for CFI stated to a group of state OCD-DRU workers during an April 2016 training session titled "CDBG-DR Duplication of Benefits, 4-7-16".

When using the SBA Loan processing procedures detailed in the SBA SOP 50 10 revision 9 and reading the transcripts from HUD CDBG-DR Training then cross referencing the SBA investors training you may get the impression that the SBA is undermining HUD's National Objectives and are placing Low to Moderate Income families at risk of losing their homes which were required collateral by the SBA. The SBA is not working in the best interest of disaster victims and completely undermining the HUD CDBG-DR program designed to assist those of low to moderate incomes.

To Homeowners looking for disaster recovery funds the SBA will qualify all your needs with your credit history or collateral alone without emphasis on the true current ability to repay.

To Investors, the SBA promotes that all disaster loans are 100% secured by borrowers collateral.

When I learned that Mr. and Mrs. Aultman were living on 90% of their monthly retirement income and their SBA Loan offer for $124,000 would add $439 per month for 30 years, it didn't take much to calculate that the 14% increase would place the Aultmans at 104% expense to income ratio and they would be filing for bankruptcy in a matter of months or forced to re-enter the job market to increase their monthly income.

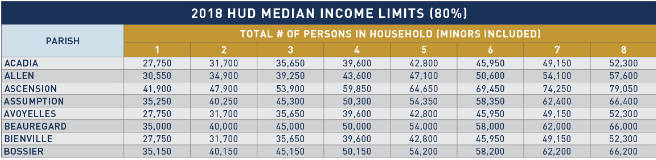

HUD vs. SBA Household Income levels to receive HUD Grants and financial assistance via the CDBG-DR Program.

HUD CDBG-DR Program is based on providing 80% of the appropriations and allocations assistance funds to the 80% AMI households in the most impacted disaster areas. Our OCD-DRU requested a waiver to lower the 80% of the appropriations and allocations to 50% and HUD countered with 55% of the funds to be used for 80% AMI families in the most impacted disaster areas.

Ascension Retiree Household of 2 = $47,900 80% AMI (Moderate income)

51% to 80% ($23,950 to $47,900) moderate income Ascension Parish.

31% to 50% ($14,370 to $23,950) Low Income Ascension Parish (SBA Loans Qualify to $20,300)

0% to 30% ($0.00 to $14,370) Extremely Low Income Ascension Parish

(IMAGE HUD 80% AMI Ascension Parish Louisiana)

Exhibit: HUD 80% AMI (Link)

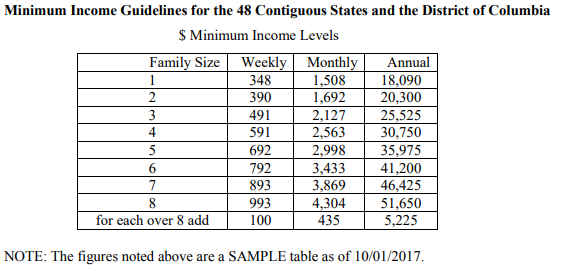

SBA uses it's own household income levels which include levels below 80% AMI. This is in direct conflict with HUD's national objective to assist 80% AMI Low to Moderate Income Households.

(IMAGE SBA Minimum Income Levels)

Exhibit: SBA Minimum Income Levels

The SBA will calculate the ability to repay by your credit repayment history and / or what they believe your future pay increases will be. For our Retirees that have a household of 2 the SBA minimum income of $20,300 qualification could set this couple up for financial bankruptcy and the loss of their home twice, once to the disaster and the second to the SBA loan program.

To calculate the ability to repay based on $20,300 pre-tax income is not what a prudent person would think is reasonable. To have loan payments over $400 per month would be unthinkable and to place a low income disaster victim in a position that they have to use their home as collateral is a formula for a second disaster, homelessness. We can not allow our Low to Moderate income households to fall victim to financial debt after the disaster, this group does not have the means to repay this debt and any rational thinking person would know this. To take advantage of a household that can not think rationally due to the disaster and the frustration knowing relief is only in the form of a loan that places their home at risk just adds to health issues and financial stress due to their debt burden.

Resources: