For Federal Declared Disasters which would be measured by major to severe damage assessments caused by the disaster event we have a mix of funding sources encompassing both public assistance and private assistance for your disaster recovery.

We are all aware of the Federal Emergency Management Agency (FEMA) which will offer more public assistance to your local agencies and state agencies than individuals and households. But that's not to say they will not offer assistance. You may need to push very hard to get someone to provide you with the path to take so you can receive assistance. Be sure to keep your attitude and anger in check when dealing with FEMA call center people and field representatives. You'll not be discriminated against but if I say you may not have someone offer more than what FEMA normally shares and you can read that on their website. So be strong with your conviction that you need assistance, be on point with who and how many needs the assistance and learn what the maximum amount of assistance you can receive is and make that your goal. Learn the difference between the grants and never take a loan until you have exhausted all other options. It's your responsibility to reduce your disaster recovery debt burden not the federal government or your local and state agencies.

FEMA is your first agency you will need to register with and get your damage assessment completed by. The FEMA Verified Loss (FVL) damage assessment will assist you in securing other funding for your recovery. Without a FVL with a determination of major to sever damage you may not be eligible for public (government) assistance and will need to look to the private sector (banks, insurance, etc.) for assistance.

FEMA = Individual Assistance (IA) and Individuals and Household Assistance (IHP)

FEMA will then send you to the SBA for a low interest repayable disaster loan. Your state may require you to file for a loan but your state can not penalize you for not applying and if you do apply you can not be penalized for not taking the loan for any reason.

SBA loans are a serious Duplication of Benefits which means if you qualify for a Grant which does not have to be repaid and you take an SBA Disaster Loan that has to be repaid you will forfeit the amount of the GRANT equal to the SBA Disaster Loan. Their is a path around this issue. If you were to apply for a private loan from a private lender or local bank the loan from a private sector lender will not be counted as a Duplication of Benefits (DOB) and you could use grants that you may qualify for to pay off your private loans. This is not information offered by FEMA because FEMA does not list other agencies in it's sequence of disaster funding. (See the chart)

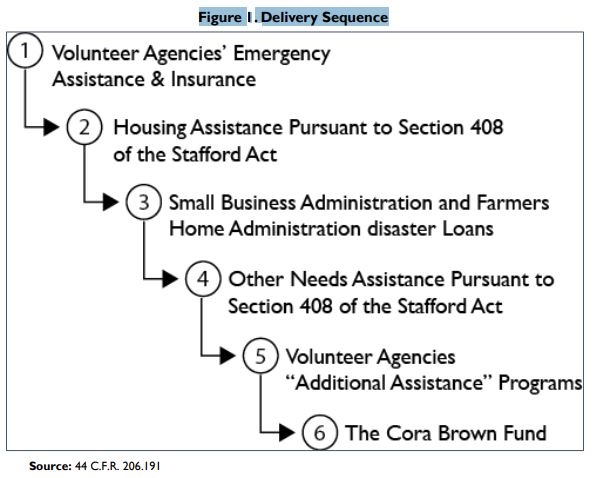

Chart of Sequence

First assistance always comes from our Faith based community then Volunteer organizations and in both cases they seem to arrive the same day of the disaster.

Next group would be our Emergency Assistance agencies and Private Insurance companies.

From that point our Housing Assistance following Section 408 of the Stafford Act helps people find temporary housing and shelters.

The Small Business Administration (SBA) and the Farmers Home Administration step in and offer disaster loans. Typically those that do not have good credit or history of good credit would take advantage of these loans. If you have been turned down from local private lenders the SBA and FHA would be who you would contact for disaster loan assistance.

If you have other needs and have not received loans or grants for these needs FEMA offers a grant program called, Other Needs Assistance which typically is offered only when you are denied an SBA or FHA disaster loan and is pursuant to Section 408 of the Stafford Act.

Next is back to the Volunteer Agencies for more assistance and Additional Assistance with programs funded by federal tax dollars throughout the year. One such agency is the United Way and Catholic Charities who will assist you in finding funds and resources for your disaster needs not covered to this point.

And final for the documented sequence of disaster assistance is the Cora Brown Fund. There is a very good story behind this fund and foundation and I recommend you take a minute to read it. Typically funding from the Cora Brown Fund are limited to specific and special cases.

Delivery Sequence (NOTE: SBA Version)

1. Volunteer Agencies Emergency Assistance & Insurance

2. Housing Assistance Pursuant to Section 408 of the Stafford Act (FEMA)

3. Small Business Administration and Farmers Home Administration Disaster loans (SBA)

4. Other Needs Assistance Pursuant to Section 408 of the Stafford Act. (FEMA)

5. Volunteer Agencies "Additional Assistance Programs.

6. The Cora Brown Funds

Secondary more detailed list: (NOTE: FEMA Version)

1. Volunteer Agencies Emergency Assistance & Insurance Hazard and flood insurance

2. Housing Assistance Pursuant to Section 408 of the Stafford Act. FEMA Home Repair and Replacement

3. Small Business Administration and Farmers Home Administration Disaster loans

4. FEMA Individuals and Households Program and Other Needs Assistance Pursuant to Section 408 of the Stafford Act.

5. Other Federal, state and local government funds

6. Volunteer Agencies "Additional Assistance Programs.

FEMA regulations assign the order to which you are offered disaster assistance. The order which I have listed above is the order that FEMA identifies as the proper federal assistance delivery sequence.

It's important to remember that a lower level agency in the sequence of delivery cannot be used to pay for a higher agencies funding. This means after FEMA and your IA or IHP grants comes the SBA loans. If the SBA offered you enough money in a loan package to rebuild and make you whole again no other downstream assistance would be offered or even eligible for your disaster recovery. Even if you were offered a grant that does not need to be repaid the SBA loan amount would be duplicate in nature of your disaster recovery and would be a negative or subtracted from any funds you may be eligible for at a later date.

The best example I would like to use is the Housing and Urban Development (HUD) Community Development Block Grant Disaster Recovery (CDBG-DR) program. The HUD program is designed to help based on annual median income (AMI) levels starting at 30% AMI but often being elevated to 80% AMI and even 120% AMI offering assistance. Each state has part of their state government an agency or department that manages all HUD CDBG-DR grant programs. These agencies can and do create policy for eligibility, processing, distribution, waivers and even what damage levels make you eligible.

At this point most of those who did not qualify for private lender loans (bank loans) and were not eligible for FEMA Other Needs Assistance (ONA) would be best suited for HUD CDBG-DR grants. But most are pushed to the SBA and place collateral up to secure the loan and become trapped with a disaster loan mostly because the homeowner was never made aware of other options like HUD CDBG-DR grants.

The HUD CDBG-DR program has to be managed by your state office of community development or any related state agency. They will be part of your Governors disaster recovery team and most are in the states department of administration. These same departments will manage normal HUD CDBG programs which every state has available to them.

Funds that HUD uses for CDBG DR Grants cannot be used to pay off or pay down SBA loans due to the sequence of delivery FEMA has in place.

FEMA considers HUD as Other Government Assistance and FEMA makes no reference to HUD CDBG-DR Grants in any of it's disaster assistance or training. This actually increases financial disaster debt burden on individuals and households, homeowners and even landlords, small businesses as well as farming, fishing and other agricultural industries. By not mentioning Grants early on in your disaster recovery FEMA pushes the disaster victim in the direction of holding the disaster recovery debt burden exclusively.

For many managing disaster recovery financially is not very difficult, with the proper amount of insurances, cash for deductibles and a good credit line for loans to cover what insurance did not cover individuals and households with good income and credit to include credit history (credit elsewhere) are faster with their recoveries and back to work earning to repay any debt they had acquired during their recovery period.

For the households managing their disaster recovery that do not have insurance or were under-insured. Those that didn't have the deductible or down payments. Those that may not have incomes great enough to take on additional disaster debt. Those living in poverty, very low income or low to moderate income have the most difficult time recovering from a major disaster. For thousands they will not be informed of the funds from HUD CDBG-DR grants that will take 6 to 12 months to be available to the state for distribution to eligible individuals and households.

Let's review once again the sequence of disaster assistance again and make a determination which assistance would be best for you and your household.

During the Emergency Phase:

During the Relief Phase:

-

Insurance

Homeowners, NFIP, etc.

-

FEMA Registration

-

FEMA Housing Assistance (Element of the Individuals and Household Program IHP)

Assistance to assist in finding temporary shelter or to make the home safe, secure and functional.

-

Small Business Administration (SBA) Disaster Loans Homeowners, Renters, Businesses.

-

Other Government Disaster Programs, Disaster Unemployment Assistance (DUA), Crisis Counseling, Legal Assistance, IRS Assistance for casualty loss, Veterans Assistance, HUD Housing, USDA Rural Housing, USDA Food Stamp Assistance.

-

FEMA &ndash Other Needs Assistance (ONA) only qualified if denied SBA loan. This grant from FEMA is promoted to those with personal property needs, transportation needs and moving and storage. The ONA program is often used as bait to make the household apply for a SBA Disaster Recovery Loan. You need to be denied by the SBA for the disaster loan in any amount before you are eligible for a ONA grant. Credit scores of 450 and above and $50 cash in hand or collateral will secure your loan with the SBA. Even if you do not have the ability to repay the loan you will most likely qualify for a typical SBA Disaster Recovery Loan.

-

Other Needs Assistance from FEMA will be available to individuals and households without applying for an SBA Disaster Loan for any of the following debts caused by the disaster, funeral expenses, dental, medical, public transportation and some other personal expenses.

-

Long Term Recovery typically only means HUD CDBG-DR programs. But some states will include voluntary agencies, faith-based organizations for your recovery. The facts are simple, most of these not for profit groups are only given funding for 2 to 3 years and do not offer enough to assist large groups recovering from a major disaster. You'll find your long term recovery will be funded via HUD and managed by your state.

HUD has issued DOB Guidance over the years and should be shared with all disaster victims by their state government in the same venue where state and local governments share FEMA and SBA information.

Knowing you have additional recovery paths can reduce the overall debt burden from a disaster on a household. Many homes are never repaired to pre-disaster condition or not repaired at all but the family continues to inhabit the structure. In some cases the home is abandoned for lack of repair funding.

We can change the disaster recovery outcome by informing more not for profit groups about the HUD CDBG-DR programs and get the material homeowners need before they register with FEMA.

Let's keep the information flowing and work with our individual congressional representatives to add HUD CDBG-DR programs to the list of disaster assistance from the date of the declared disaster. If we can have allocations available at the same time FEMA is authorized to start Public Assistance we can speed up the recovery time for those most in need that typically wait 2 to 3 years before repairs are even started.